The Big Picture

The Federal Reserve cut interest rates by a quarter point last week in an effort to inject energy into the housing market and the broader economy. The cut followed weak inflation and job data.

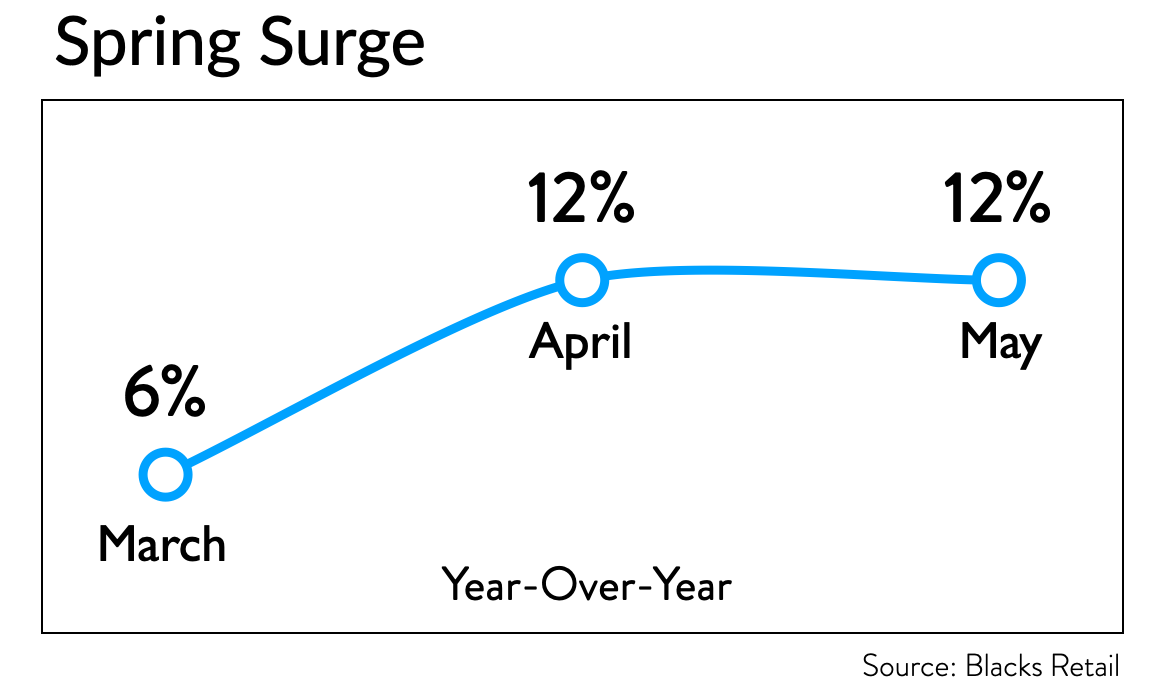

While the macro numbers looked shaky, retail showed surprising strength. According to the Commerce Department, overall sales rose 0.6% in both July and August, proving that consumers still have money and the will to spend.

August Performance: Fashion Leads

Our client stores didn’t just ride the wave—they outperformed it.

July delivered the strongest summer we’ve ever recorded, up 11%.

August held momentum with an 8% surge, fueled by demand for early fall arrivals.

In women’s apparel:

Ready-to-wear powered an 11% increase.

Dresses climbed a steady 4%.

In men’s apparel:

Soft coats skyrocketed 46%, signaling the return of elevated dressing.

Fall sweaters gained 21%, while bottoms remained a standout: casual pants jumped 23% and dress pants rose 13%

Spring Outlook: Cooling Momentum

Fall got off to a red-hot start, but September has slowed as shelves look picked over and shoppers have already grabbed the season’s newest looks. Looking ahead, we’re forecasting a moderate spring.

The wildcard remains tariffs. Holiday performance will determine how shoppers respond when pre-spring goods arrive priced 10–30% higher.

Here’s the risk:

If prices rise 20% but sales only rise 15%, profits erode. Higher inventories turn into markdowns. This is particularly dangerous for fashion stores, since unsold goods rarely carry into the next season.

Retailers face a tough choice: offer basics that carry over, or double down on newness. This summer, consumers gave us the answer loud and clear: they want new looks, not repeats.

Blacks’ Bottom Line

The only way to keep delivering the freshness customers crave without drowning in excess inventory is to turn product faster.