The Big Picture

Overall retail sales rose by 0.4% last month, coming in equal to the increase in consumer prices. This means that consumption barely caught up with inflation. Although inflation is easing, it is still a factor affecting consumer confidence, which fell to a nine-month low in April.

Meanwhile, the Census Bureau reported that sales in fashion specialty stores were down 0.4% for the first quarter of this year, while department stores fared a bit better, posting a 0.6% gain. These are disappointing results for the wider market but do not reflect how our higher-end specialty retailers have been performing.

Sales overall have proven to be somewhat resilient, but all eyes are now on the debt ceiling talks, and whether a deal is reached before the U.S. defaults, leading to a potential worldwide crisis.

April Sales

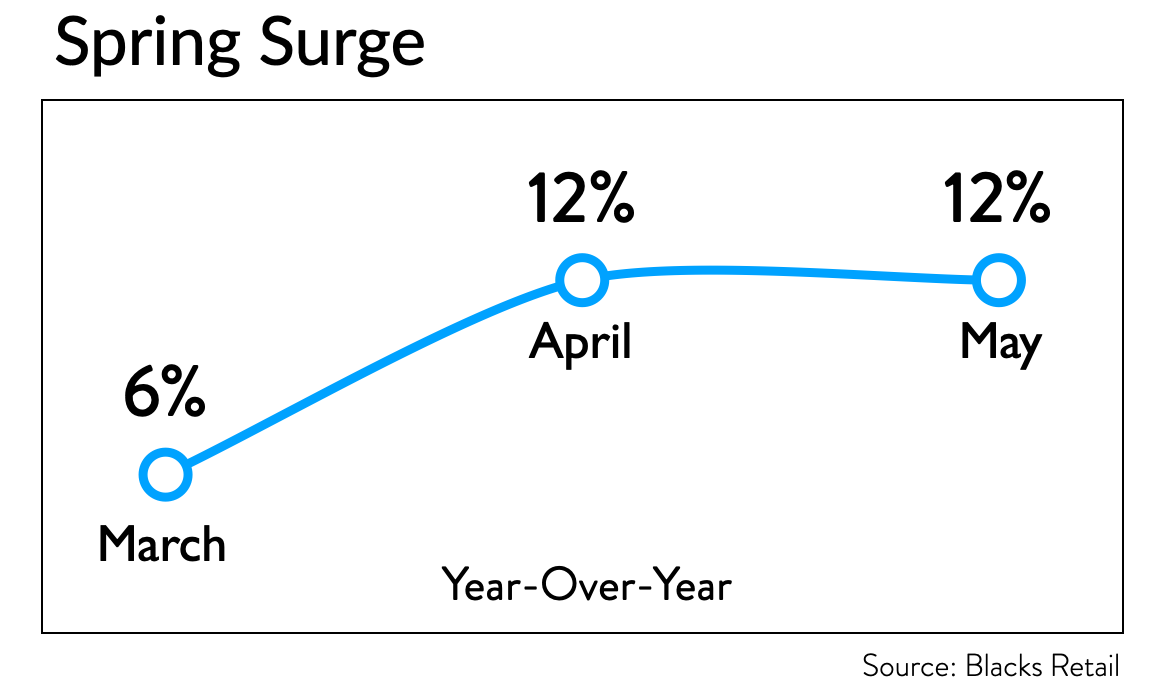

Among our client stores, April sales improved over March, which was one of the weakest months since the pandemic recovery began.

Women’s wear was down 2% overall from last April, while menswear saw a 6% drop. It’s worth noting that we were going up against some of the highest year-ago figures we’ve seen; sales on average last April were up by 50%.

One standout category for both menswear and women’s wear was Special Orders, which were up 6% and 23%, respectively.

What’s more, early May sales figures show an even more dramatic improvement. When we tally the final numbers, we could be seeing a surprise bump like we saw in January.

Looking Ahead

Given the uptick we’re seeing right now, we might not have to take as many markdowns when we reach the summer months, but we will have to play that by ear. In general, we are seeing markdown levels normalizing from the lows of 2021 to 2022.

So far, customers are accepting the price increases that vendors have passed on. However, customers have not seen the Fall ‘24 merchandise yet, so this could be when they get a little sticker shock.

For this fall, we are going against somewhat softer year-ago numbers, so it shouldn’t be too hard to meet or beat last year given the current momentum. Spring ‘24 should also be relatively easy to meet. The challenge will come in Fall’ 24, especially given that it’s an election season, which can be tricky.

On the fashion front, one of the concerns we have is the emergence of “quiet luxury” (see pic above), which doesn’t seem to have any driving brand or trend influence. Without “must have” looks or items it’s hard to get customers excited to buy more if they already have a full wardrobe.

Blacks’ Bottom Line

A lack of fashion could make it more difficult to get repeat customers in the seasons ahead. This means it’s more important than ever that vendors get “loud” with luxury again. Be on the lookout for solid trends when you go to market.