The Big Picture

Just as we were reaching greater stability amid the pandemic, the escalating war in Ukraine has reintroduced uncertainty into the market. The stock market has dipped as oil prices have surged, and consumer confidence has fallen to an 11-year low. The loss of confidence is mostly due to rising inflation, which clocked in at 7.9% in February.

As the Russian invasion of Ukraine wears on it will continue to affect the energy sector, causing prices to rise across the board. Just how long consumers will bear these rising costs remains to be seen. That said, we have still not seen a slowdown in any of our client stores. In fact, sales for the first 90 days of the year have exceeded expectations.

February Sales

Overall retail sales grew by 8.7% in February compared to the previous year, and sales were up 17.3% against 2019. This data, from MasterCard SpendingPulse, mirrors what we saw in our stores.

Consumers continued to buy throughout the normally slower post-holiday months of January and February. What’s more, our merchants took fewer markdowns than they did in previous years, allowing them to gain more margin.

And so far in March we have continued to see strong demand, despite market volatility. This bodes well for the spring season, which we planned up by low single digits.

Fall Plans

For most stores, we have been planning small sales increases for fall over 2021. Initially we planned them up by around 6%, but after seeing such a strong performance in March we expect those increases to grow to 8%.

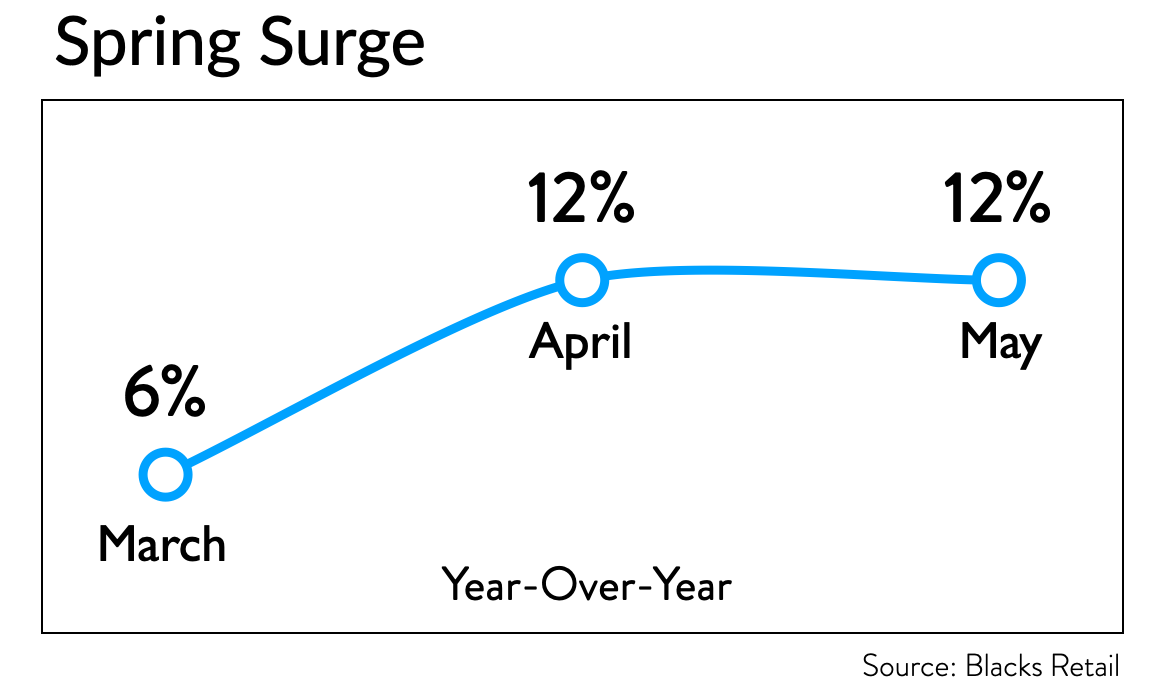

We are keeping a close eye on the April to May period, however, since we believe it will be a bellwether for consumer demand going forward. At that point we should know whether world events and inflation start to take their toll.

The good news is that the fall product looks great. Sport shirts, shirt jackets, and over shirts represent strong trend opportunities in menswear, so merchants should definitely invest in these areas.

In women’s wear right now it is all about dresses – both daytime and evening dresses are selling quickly.

We are also seeing a resurgence in the jacket business (many times they are classified as Blazers, but don’t get hung up on the category name.) Look for novelty, since the category is set for major growth as we transition into the pre-fall/fall selling season.

New silhouettes in Jeans are also performing very well.

While we are keeping a cautious eye out for any changes in the wider market, consumer spending overall has not decreased. And given that many stores are beating their sales plans so far this year, we are advising clients to be bullish going into the fall season.

So, if you normally hold back 20% of your open-to-buy for in-season purchases, reduce that to 10% or 15% and get the goods you need upfront. Supply chain issues are still lingering so you may not be able to get the extra goods in season, and you will likely sell through the extra inventory bought up front.

Blacks’ Bottom Line

When it comes to fall planning, be bullish. We’ve haven’t seen any signs that consumers are satiated yet.